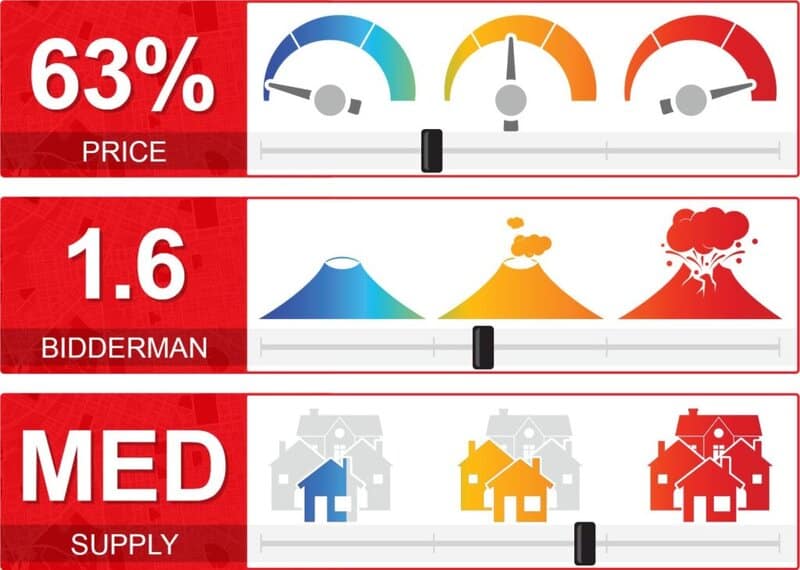

100 Auction Test is where we randomly select Top End homes before they go to auction and then we turn up and report on all results, so as you can get a true picture of the current Inner Melbourne Top End Market. We do it 4 times a year in the major Top End markets, over the same 3 week period.

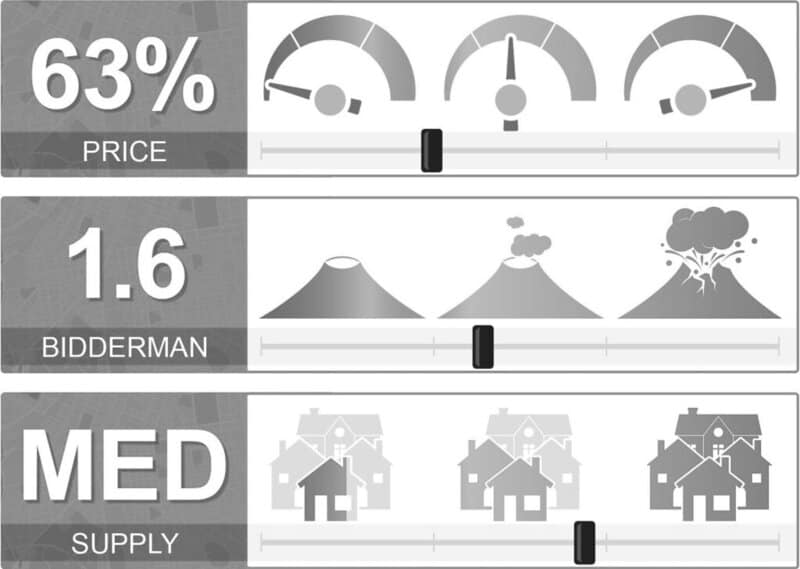

Demand – Bidderman. How many bidders per auction? A very accurate measurement of market depth when taken over a wide sample. Number of Bidders / Number of Auctions.

1 bidder average – Falling Market. 2 bidders – Rising Market. 3 bidder average – On Fire

Supply – Stock Levels. It’s a nuanced opinion measurement, more so than scientific, as there can be a flood of unrenovated homes, but the market wants ready to move in.

Clearance Price % – Many data points give exaggerated readings as agents choose to leave out the bad news (unsolds). We choose the sample before auction and track down every result. The higher the clearance rate, the more agreement between buyer and seller on price and if Bidderman is also strong this shows prices are rising.

Measurements: Under 60% falling. 60-70% some stability. 70%-80% rising. 80%+ On fire.

Opening Market usually sets a direction till Easter (sometimes the whole year)

May Market post Easter leading into Winter trends – capricious market usually.

Spring Market is Footy Finals and Pre-Cup – a major buy sell season. Can see a market turnaround either way, coming out of winter.

Christmas Market is from November till Santa comes. Often the hardest market to sell in, due to oversupply relative to unsatisfied demand.

GLOSSARY

PPP’s – All homes and all buyers have 3 characteristics. A good deal for a buyer is when their PPP’s match the homes PPP’s.

Position (land location) + Property (building) + Price = 3P’s. A buyer can adjust all three to get what they really, really want and to meet the market.

Whilst a home has 3 P’s, a seller has only 1 P they can adjust – Price. Although a good seller and agent can, prior to the sale, affect the P of Property through Presentation.

Overall there are 3P’s and Position is most often, the most important.

A-Graders – If the home’s PPP’s are desirable to many in the market we call that an A-Grader. However, it’s all the 3P’s that need to be desirable. You can have a great location, great building and be overpriced in which case you have only 2 desirable P’s – we call that a B-Grader. C-Graders have 1 or no desirable PPP’s and the only usual desirable P is Price – a weak one – this is why C-Graders are poor investments.

Volcanoes – When the market is hot you see increasing numbers of 4 or more bidders on homes. We call that a volcano. 1 or no bidders we call a duck.

Wounded Underbidders – Buyers who miss, go harder (more money) next time to avoid the hurt of missing out again. When there are multiple unhappy buyers, who have missed multiple times (wounded underbidders), the market rises quickly.

Cautious Buyers – Non-Bidders – Potential buyers who see lots of pass-ins, tend to not want to bid because their fear of overpaying is greater than their desire to buy and get out of the market.

Stales – Number and length of time a property remains unsold. The older the stale, the weaker the price (as a general rule). The more stales, the weaker the market as they clog up the market creating an oversupply.

Off-market – Homes that are for sale but are not advertised in the mainstream media like realestate.com.au. Over say $5 million there are considerably more homes off market than on market. More than ½ the homes we buy and sell are off-market.

Pre-market – Homes that some agents say are Off-market. Pre-market homes are homes coming to market but are not yet advertised and are often not really for sale at the moment.

On-market – usually refers to homes sold with major advertising say on Domain or realestate.com.au

Not for sale (and the 4 ducks) – there are many homes that are also said to be Off-market or Pre-market homes that are not really for sale. Why? Seller is testing the market. Agent is testing the market. Agent has no work. Seller wants a free valuation or some company.

For a home to be really for sale off-market, it needs to pass the 4 Duck Test.

- Agent Authority

- Contract of Sale

- Asking Price

- Easy Access.

Good ól Boring Process – When you are cooking a cake – do you get your best results by making up the ingredients, the amounts and throwing them into together, hoping for the best? If you do great, but I’m not hungry. A good recipe is a good process. And in property a good recipe is 3 Questions starting with what do I really really want? If you can’t work that out, then engage a good agent. When you answer that question, you go to the 2nd and 3rd questions and make good decisions. Good decisions lead to good outcomes – for you.

Market Prices – Every price is supposedly a market price. It’s a lazy concept.

Market price is a living organism – lets imagine it’s like a human. The market is the blood, the circulatory system. The PPP’s are the bones, the skin, the main organs and we agents and agent marketing are the lipstick, perfume, clothes. All 3 – blood, bones and lipstick make up a price and its attractiveness, it’s not just the market.

Market Values – Values are opinions. All opinions have vested interests and biases. What the council, the bank, the agent, the buyer, the seller values a home at will all be different.

Last year two valuers came to a home I was looking to refinance – $4m home – 3 weeks apart the valuations were approx. $700,000 different – that’s qualified valuers – same criteria.

Market Value v Market Price – One is an opinion before the deal and one is the actual result after the deal.

Quote Range: It is thought to be an agent estimate of final price – it is not. See Quoting

Under the Hammer: is when a home is sold to a buyer under the auctioneer’s hammer that is on the street or in the home in front of crowd when we says sold – it can be just clapping his hands together – under the hammer refers to the old gavel now only sometimes used.

On the market: (different from on-market) is a colloquial term that an agent or auctioneer uses to state we are now at a level that it will be sold (now) even if there is no more bidding.

What affects markets?

Demand and Supply – yes sir re – that is what really affects markets.

Some Key Supply Variants

- Government restrictions

- Lag Times in supply of demand changes

- Builders and materials

Some Key Demand Variants

- Money – Bank credit and community wealth

- Overseas Buyers, Interstate Buyers, Migration

- Stock Markets and World Events

Predicting the Future

Economists, banking leaders and other market predictors are like horse race “experts” – entertaining but of little long-term value. In 2017, 2018, 2019, 2020 the pundits on where the market was going got it wrong, dead wrong 4 from 4. A coin toss should have got at least 2 from 4. The only pundit we listen to with respect, is the one that says they don’t really know.

Rising / Falling / Easing – Humans are herd animals.

When there are a number of pass-ins the market eases. When combined with increasing stock coming on and more stales, the market falls more sharply.

Increasing numbers of wounded underbidders and less stock the market edges up – when wounded underbidders combine with loose bank lending and tight stock and increasing migration, then market prices begin to run away.

A home can easily be 5% more or less in a week (1 bidder drops away) and parts of the market can change by 5% in a month. A property can change by 10% during the length of an auction campaign. It is very similar to the ASX in terms of its variability – it’s just not as transparent.

Individual property prices are very fluid, they are far from fixed as many think and claim.

Mexican Waves: Occur at least twice a year – Labour Day to Easter and Footy Finals to the Cup.

It’s about the Ultra Top End, where agent led PR stories begin to appear in the papers, at the end of your phone and on social media; with the point of creating some momentum selling of trophy homes.

It’s a Mexican Wave; a powerful force that lives in the Top End of Melbourne real estate, dormant for much of the time, only to suddenly awake, just as it does at the G.

The Mexican as we call it and how it works.

1.Opening Stanza are side of mouth whispers about what may be coming to market quietly.

2.The Build by the protagonists is a balancing act of credible rumours (sales & prices behind closed doors) with the reality of what the punters can see on the street (sold stickers).

3.The Crescendo ….the results incited (or not) are almost secondary to this living, moving organism ……… however as quickly as it rises, the puff can drift and the intensity drop ….. and so, it lies dormant again until circumstances reignite life ..…. the next time around.

A good Mexican starts gently with some lite prosaic gossip. It is then fostered by those few Ultra Top End agents, who know the proven repetitive actions. They have a passion plan to finish with magic ……… screaming emotions, hands in the air and index fingers on computer screens ……. some on market but most silently (until cooling-off is over) off-market.

The latest result or near miss becomes a new side of mouth whisper and the wave restarts.

A good Mexican highlights the craftsperson’s art of luminating with innuendo a grey path that points to a light in the distance. This illumination brightens as the industry works together (consciously and subconsciously) even though they have competing interests, even though their comments differ, even though in many cases they dislike each other….to show all buyers and sellers where that light really could be, for each buyer and seller.

A living thing of wonderment is clarified during this time. Last year it launched itself into the stratosphere at Easter and again just before the Cup. For the previous few years, others have not left the launch pad or cruised at far lower altitudes until their power faded.

The Mexican with this bi-annual wildebeest migration timing will have either a La Niña or El Niño filtering effect on the rest of the Melbourne market in 2022, as it does each year.

In 2022 if like an MCG Mexican it builds again, then all of us will walk a little taller – as we all like to be in the presence of a bigger force at Melbourne’s Top End.

So mujeres and hombres crank it up and give us some good stories. Good stories for buyers (releasing of new stock), good stories for sellers (offer momentum) and good stories for the rest of us (dreams can still happen).

Market Conundrum – often the best time to buy or sell is when everybody else doesn’t want to – eg counter to the markets.

Buy or sell timing maxims we live by? Assuming it’s an A-grader. If you really, really like it, buy now. If you really, really like it never sell.

Which brings us back to Doe. Doe is dear, a female deer. This is why 10,000 people read Marketnews.com.au. It’s the only property thing that makes no sense (smiley face).

Underquoting – is when an advertised price (an agent quote) is below one of

- Agent estimates of value or

- A written buyer offer or

- The Vendor reserve

An agent quote is not a valuation, it is not a fixed sticker price – a quote is seen by my industry as a vehicle to attract bees (buyers) to the honey (home) and that’s ok, if legal.

However underquoting is unethical but widespread. Underquoting has been endemic in the last week of an auction campaign in the markets of 2015, 2016, 2019, 2020 and 2021 – a new falling market may be different.

Underquoting is a badge of honour for some selling agents – for god sake there is cheering from the rafters with every $1,000,000 over reserve. It’s celebrated not put into balance or condemned in the media. Please note sometimes genuine market forces create $1,000,000 over reserve when it’s not an underquote (celebrate then) – but when it is happening week in and week out and to the same people and same companies, then they must be very unlucky or incompetent agents or they are serial underquoters.

Underquoting can work in a rising market – work for the agent and seller that is, not the buyers.

Underquoting can hurt inexperienced buyers in 4 bidder auctions BUT

In many instances in falling markets and with B and C Graders it actually hurts the sellers – e.g. duck or 1 bidder auctions.

Underquoting is fixable with a buyer education program as to what a quote is and what it can and cannot do AND moveable (not fixed) step up and step down written legal quoting AND timely stated auction reserves say ? days out from an auction AND mostly an industry desire, but there is minimal desire within my industry or the CAV or the government.

Legal Step Quoting: A term we invented to explain moves/strategies in quoting. We used to have a problem with it, but now we see it as sensible practise on behalf of the seller – so long as it is down legally and actually done. Step quoting if done legally is simply moving the written quote during the campaign in line with offers, changing or firming vendor reserves and any changing agent’s opinion of likely value.

Illegal Step Quoting: Is when the agent has a written quote, then tells you a higher quote on the phone and then an even high quote after you offer.

Legal Quoting: It is legal (and we consider ethical and professional) for the agent to quote above the seller’s reserve providing it meets the other two key criteria.

Legal Quoting: When it’s on the market and unexpected market forces take it well past expectations. Our only argument is how often can that happen to one agent or agency before it becomes obviously illegal.

Argy-Bargy – How can a seller ask for more after a pass-in than the quote? It’s a grey area, as CAV says its completely legal.

If it’s below the top of the quote and passed in – then it seems like all bets are off for the buyer and seller to ask and offer whatever they like to reach a deal in their best interests.

If it’s at auction and above the quote then it may be legal, but we consider a pass-in above the quote wrong. It’s a Clayton’s Quote (the quote you have when you’re not telling the truth).

A pass-in above the quote and no sale to the highest bidder is in our opinion wrong on so many fronts (morally), but CAV says it’s ok legally (go figure).

Quoting even with the best intentions (and we have them) is not a perfect science, just as market valuations and your buying estimates are not.

All our most recent sale managed selling campaign quotes.

Range: On market and Sold 1% above the range.

Range: Sold 1% below the quote range

Range: Sold within auction quote range after step quoting to vendors changing reserve

Range: Sold at EOI (Volcano) – 5% above the range

Range: Sold after auction within the auction range

Range: Sold within the range

Range: On market in range and sold 11% above the range (Volcano)

Range: On market 1% above range and sold 5% above the range

Range: Sold within the range

Single Price: Sold within 3%

Range: Sold within the range

Single Price: Step quoted down off-market and sold within 2%

Range: Sold within the range

Range and we auction step quoted up: Sold within the final week range

Range: Sold 2% above the range

Range: Sold 3% above the range

Range: Sold 13% above the range

Range: Sold within range

James Buy Sell Process – Ethical quoting brings more real buyers and sellers to you:

Early Campaign: We quote to attract buyers but not below what we reasonably think the home may go for. Where the seller has a firm price, we do not quote below that price either.

We suggest the seller keeps an open mind on reserve (early days) if their main focus is to sell.

If the seller has a firm fixed reserve and it’s too high, then not only will he or she be unlikely to sell but he or she will get no feedback on price and therefore he or she could compound the selling issue down the track – a double negative for selling – eventually getting a lower price.

Middle of Campaign: We may Step Quote (change the quote, preferably up, but sometimes down to more accurately represent the sellers thought on possible reserve and/or feedback from buyers and/or if we have had an offer that has not been accepted)

Advertised final week of Campaign: We genuinely try and have the quote reflecting a seller reserve and where James Buy Sell now thinks the majority of buyers are. Please note: it is not an exact science, and we cannot predict all buyers (often buyers do not tell the door agent anything or say lower amounts – both sides can be guilty of misrepresentations).

We care about buyers and our quoting reputation. If you do a building inspection in the last week of the campaign and the reserve ends up outside the quote, please ring us and we will probably refund any professional building inspections up to $600.

T

he current Underquoting enquiry’s timing relates to a forthcoming election, is running into a falling market where underquoting is less noticeable.

The best way to deal with underquoting (currently) is through your own quality research or a quality buyer agent or if selling then an ethical selling agent.

Buying and selling in less than half the market click here to find out more?

Are your Reports Values Strategies evidence based?