August 11, 2026

The Market Isn’t Just Slow

It Feels completely different! It Feels like its Fundamentally changed!

The 2026 Mid-Year James Report

Part One — The Structural Reset

What we think we’re seeing across prestige Melbourne, from the streets rather than the spreadsheet.

Over the past six months — walking the streets of Melbourne, sitting at kitchen tables, bidding at auctions, negotiating behind closed doors, and advising buyers and sellers across the city — we’ve increasingly come to believe that the volatility we’re seeing in the prestige market is not temporary anymore.

We think this is the new norm.

And this report is really an attempt to explain what we think we’re seeing out there.

Not from an economist’s desk.

Not from headline data.

But from the lived reality of buying and selling prestige homes across Melbourne right now.

At its core, we think the prestige market’s gravitational pull remains incredibly powerful.

People still aspire to better homes.

Better streets.

Better lifestyles.

That emotional desire has not disappeared.

But the wealth architecture underpinning that desire has changed dramatically.

Economically, you could say:

“The prestige market’s gravitational pull remains emotionally powerful, but the wealth transmission mechanism that fuelled its previous orbit has structurally weakened.”

That’s the economist version.

In plain English? The desire is still there. The money underneath ain’t.

Through most of the last 30 or 40 years, Australia operated with several powerful tailwinds underneath property. Population growth was strong. Wealth was broadly increasing across most age groups and classes. Migration was high. And increasingly, Australia — and Melbourne in particular — became an international destination for wealth.

At the prestige end, that mattered enormously. Because even when local affordability was stretching, there was often another layer of capital underneath the market, supporting prices higher.

Particularly from Asia. Particularly from China.

Ten years ago, FIRB applications were everywhere. Around 30,000 nationally.

Today? It’s basically a trickle.

In fact, when was the last time you even heard somebody mention FIRB in a serious prestige property conversation? For us, it’s been years.

We don’t particularly want to argue here about why all this has happened. That’s a political discussion. This is about observing what is happening.

And what we think is happening is this. For the first time in decades, we no longer seem to have a younger or emerging wealth cohort beneath the prestige market with the same growing financial capacity to absorb the assets above them.

The aspiration remains. But the financial depth beneath it has weakened.

That matters enormously in a market fundamentally driven by demand and supply.

And we think this has been unfolding for some time. Arguably since around Cup Day 2021. But first COVID distorted things. Then interest rates dominated the narrative. Then wars. Then taxes. And meanwhile, underneath all the noise, the structural foundations kept quietly shifting.

We are ageing as a nation. Birth rates are well below replacement levels. Productivity growth feels weaker. And politically, culturally and socially, Australia increasingly appears conflicted about migration itself.

Again — not about whether those things are right or wrong. Simply about recognising what they mean for prestige property.

Because at the top end of Melbourne — where we live, where we work, where we negotiate every week — values are heavily influenced by the depth of wealth coming underneath them. And right now, that depth feels thinner than it once did.

Which is why we no longer believe what we’re experiencing is a temporary blip.

We think it is a structural reset.

But importantly, this is not a negative report. Quite the opposite. Because once you understand the market you’re actually in — rather than the one you hope you’re in — better decisions become possible. Better buying decisions. Better selling decisions. And ultimately, better family decisions.

That, really, is what this report is about.

In Part Two, we’ll show you what the reset looks like on the ground — two homes, bought in the same week, a million and a half apart from expectation, in opposite directions.

The 2026 Mid-Year James Report

Part Two — A Tale of Two Auctions

The structural reset, in two homes bought the same week — one $1.5 million over expectation, one $1.5 million under.

Today was a tale of two auctions.

In Parkville, our clients bought a home quoted at $2.8 to $3 million. We paid $4.5 million — $1.5 million above the top of the range.

In Brighton, other clients bought a home originally guided above $7 million. We secured it for $5.775 million — again about $1.5 million from expectation, but this time below.

Two prestige suburbs. Two opposite outcomes. Same week. Same market. And both were bought before auction day even arrived: Parkville on the Wednesday, Brighton on the Friday.

To us, these weren’t random outcomes. They were the new prestige market we described in Part One, made real — where emotional demand stays incredibly strong for the right homes, but financial depth has become far more selective, more nuanced and more uneven than it once was. And because we spend our days both buying and selling, sitting in both chairs, we see that divergence clearly.

Parkville

“How could you possibly pay $1.5 million over the odds, Mal?”

We didn’t. We simply believed the market’s emotional response to that particular home would be dramatically stronger than the agent’s quote reflected.

And to be fair — for every home like this, there are many more going the other way, where an owner’s or agent’s emotional value sits far above what the market will actually pay. That’s today’s prestige market.

When we first walked through with our clients — people we’d known all of two weeks — we said it plainly: we honestly believe this home could be more than $1 million undervalued. Not because the market is booming. But because it had what we call emotional architecture — qualities that resonate deeply with a small but very powerful buyer pool.

Families still want these homes. Deeply.

On the Wednesday before auction we offered $3.1 million with a five-hour deadline. You could feel the emotional temperature rising. The vendors accepted the structure — but during the deadline period, two more buyers emerged, prepared to compete on-site. Not what we hoped for, but not unexpected.

An hour before the 3pm deadline — which had now turned into an at-the-home auction — we sat our clients (I&R) down and said honestly: we do not believe your current limit of just over $4 million will buy this home.

That is not an easy conversation. But it proved correct.

The bidding opened between the two competing buyers and moved quickly from $3.1 million into the $3.3s. Then the third bidder fell away. What followed was a contest of rhythm.

Our competing bidder moved in tens. We moved in hundreds. …of thousands.

He would go $3.31 million. We would go $3.4 million. He would move ten. We would move one hundred. …of thousands.

Eventually he jumped aggressively at $4 million. We paused, consulted our clients, regrouped, then carried the contest all the way to $4.5 million. There was visible hesitation around $4.2 million — always a meaningful signal — but it still took another $300,000 before they were silenced and the property secured.

All over within minutes.

An interesting thing? The home had last sold 46 years ago for around $100,000. At $4.5 million, that’s a long-term compounding growth rate of about 8.8% per annum. This is where most people think average Melbourne growth sits today. It is not.

Brighton

Brighton sat at the opposite end of the same market. Good home. Good address. Originally guided above $7 million.

But for our buyers, there were practical compromises that materially affected value. No lift. Three levels. Complex driveway access. Our clients were in their seventies – young 70’s hey C&J. Those compromises mattered.

So instead of reacting emotionally, we worked methodically. Builders’ quotes. Lift advice. Pest and building. Legals. And throughout, we kept saying the same thing to the agent: we are not buyers in the sevens. We are not buyers in the sixes. We are buyers in the fives.

By Friday we reached a verbal agreement around $5.75 million. Then came another very human part of today’s market: the seller simply struggled to accept where the market really was, and would not sign. Another twelve hours passed, negotiating over the final $25,000, before contracts were signed at $5.775 million.

You could genuinely feel the pain on their side. But it was strong work by the agent to hold it together and get the deal done. Otherwise it simply becomes another unsold prestige home.

And perhaps that is the point. Two homes. One roughly $1.5 million above expectation. One roughly $1.5 million below.

This home had last changed hands in 2010 for about $3.85 million. At $5.775 million, that’s annualised growth of only around 2.6% per annum over fifteen years. Anecdotal — but revealing. Two prestige homes. Two entirely different long-term growth trajectories. A very succinct illustration of what has changed beneath the prestige market.

How can both be true at once?

Because the prestige market is no longer moving uniformly in terms of property types, price segments and times held.

The very best homes — the rare ones, the emotionally resonant ones — can still ignite extraordinary competition. But many prestige properties are now finding the broad financial depth beneath them is simply not what it once was. The gap between emotional desire and financial capacity is widening.

That does not mean prestige property has lost its pull. Far from it. Both of these homes were bought for families — two of four we secured for clients this week. The aspiration remains incredibly real.

But pricing outcomes now feel increasingly tied to precision, suitability, emotional resonance and genuine scarcity — rather than simply riding a broad upward wave. And, of course, there’s always some luck involved.

That is the practical reality of Melbourne’s prestige market today.

In Part Three, we turn to the numbers — and why the ones you’re being shown don’t match the market we’ve just walked you through.

The 2026 Mid-Year James Report

Part Three — You’ve Been Reading the Wrong Numbers

How months — years — of misleading data push buyers to overpay and sellers to overprice, and never understand why.

Part One was about the wrong growth numbers — what your home is supposedly worth.

This is more than that. Because you’re also being fed the wrong success numbers — whether your home will sell at all. And that one bites harder, and faster.

For a long time now, both have been wrong. And the decisions you make on the back of them are hurting you — buying or selling. As a buyer, you can pay way too much. As a seller, you can ask way too much, sit unsold for months, and never realise you never had a chance. Same bad map. Two different cliffs.

Here’s the better news. Both are navigable. We work both sides of this market — buyers on some deals, sellers on others — and on the streets of Melbourne right now, that’s exactly what we’re doing: helping people read it properly and make better decisions, short term and long. But you don’t do it on a fictional number. And you rarely do it alone.

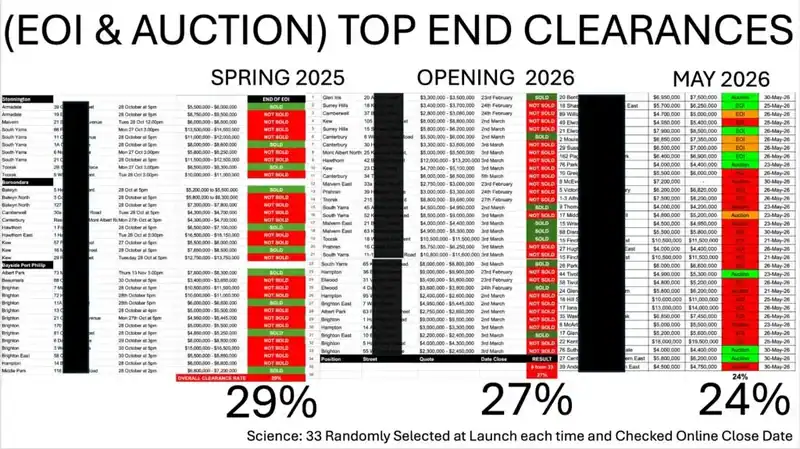

Look at the three numbers

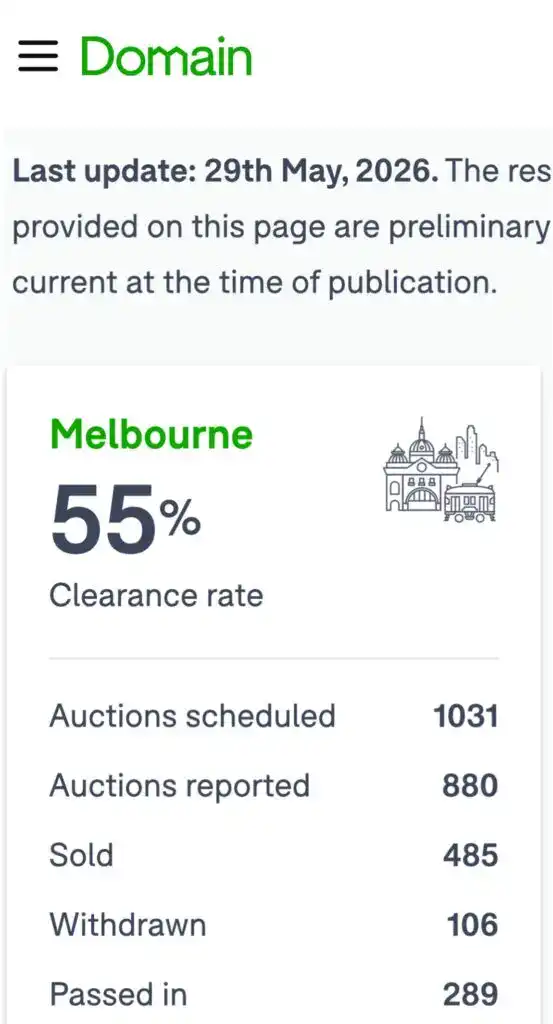

The REIV — the professional agents’ body — puts the clearance rate at near three in four. Around 73%. Hunky dory.

The same agents feed their data to Domain, the largest property masthead. Domain puts it closer to one in two. Half of all campaigns not selling.

And us? From our own numbers, on the streets of Melbourne, deal by deal? We think it’s closer to one in four. Which means three in four are *not* selling.

Three in four. One in two. One in four. The same market, described three completely different ways.

73%. Hello?

And then a stat you never see — but here’s our data. Of campaigns that fail and come back to market, only 4% — about one in twenty-three — ever achieve even the same price the second time. Almost none achieve a better one. So when a seller is told to “wait and try again,” the odds they’re being sold on are almost imaginary.

Because numbers shape behaviour

Tell a seller they have a three-in-four chance and they believe the market is healthy. So they spend — advertising, styling, portal upgrades, tens of thousands of dollars — on a market that was never there. The real odds were one in four. And when it fails, the same number that misled them gets used to wave it away as bad luck.

If that keeps happening, you have to ask: is there a class action coming for those who parlay these stats?

Tell a buyer the market is broadly strong and they can’t see what’s happening underneath — that this is a divergent market, where one home draws a crowd and the next draws no one. They read competition that isn’t there. They pay for value this market will never return.

Same fiction. Both sides hurt.

And the swings are not small. Do you know how to pay $1.5 million more when a quote has your dream home underpegged — or $1.5 million less when it’s pitched too high? That’s a $3 million spread on a $10 million budget. Thirty per cent. Wow. That gap is the whole game — and you do not navigate it on a clearance rate that was never true.

And the marketing makes it worse

The portals charge more and more, and deliver less and less, because they can. We’ve seen tens of thousands of dollars spent on portal and print advertising and not one person walk through the home. Not few buyers. Nobody. And then a report arrives celebrating “30,000 views.” Thirty thousand supposedly looked. Nobody came.

So what exactly are we paying for? Money spent to feed the same illusion — activity dressed up as demand, sitting on a number that says the market is fine.

None of this is separate from the structural reset. It’s the same story. The wealth beneath the market has thinned. Demand has lost its depth. And the published numbers either haven’t caught up, or won’t. The market has moved. The story we’re told about it hasn’t. That’s the disconnect — not between buyers and sellers, but between memory and reality.

So what does honest and helpful look like?

You need the right people and the right process — because a 30% swing is decided by judgement far more than luck. And we’ll be honest: even we don’t always get the price exactly right.

Take Albert Park. 30 Draper Street. On the market at $2,650,000, under the hammer at $2,800,000.

I got Parkville and Brighton right. I got Albert Park wrong — I had it in the low $2s.

And that’s the point. It is not about being the God of Price, always right. That’s impossible. It’s about having a good process: multi-agent, peer review, listening to others, and a strategy of testing before negotiation.

For our sellers, that means multi-agent campaigns and off-market testing — reading the real buyer pool before committing tens of thousands, and protecting a vendor from a public, failed campaign.

For our buyers, it means agent ratings, peer review and strategic price testing — pressure-testing what a home is truly worth, so you don’t pay for competition that isn’t there.

And it works. A sharp campaign in Blackburn this week — following on from a buy we’d carried out for the same clients (A&S) — one standout buyer, sold above quote before auction. Good agency, from an agent selected through our multi-agent process: Wendy Zhou, from Tim Heavyside.

It’s why we stay picky. Of our last ten campaigns, nine sold — 90%, while the wider market runs under 50%. Not magic. We tell people the truth before they spend, not after.

Because real estate in 2026 is so much more than AI, tired agents and bulldust commentary. Well — it is, if you want to get it right.

Get smart before you sell — not after a failed first or second attempt. Because one in twenty-three is not a plan, and as you can see, time does not heal mistakes in 2026 and beyond.

So, honestly

If a campaign has struggled, hear this. Yes, it can be the market — it’s probably not your home, and you’ve done nothing wrong. But increasingly, a struggling result comes back to your choices and your decisions: the people you pick, the process you run, the price you set. Those choices are almost impossible to make well when the numbers in front of you are fiction — and far easier with someone who reads both sides of this market sitting beside you.

Three in four. One in two. One in four. Half a year in, the last one is the truth — and it’s the number we’d want every buyer and seller in Melbourne to carry.

In Part Four, the practical part: what to actually do — buying and selling — and the homes we bought this month.

Who is right on Clearance? Agents 75% | Media 50% | James 25%

Address: 30 Draper Street, Albert Park

Auctioneer: Oliver Bruce Crowd: 50

On market: $2,650,000

Under hammer: $2,800,000

Bidderman: 2

This is why you need good process and good people to get good prices. I got Parkville and Brighton right but I got Albert Park wrong. I thought it was worth low $2’s

Its not about being the God of Price and always right – that’s impossible. Its about having a good process which includes multi-agent, peer review, listening to others and a strategy of testing before negotiation.

The 2026 Mid-Year James Report

Part Four — Buy Well, Live Free. Buy Poorly, Pay the Bill.

The practical one: what to actually do, whether you’re buying or selling.

So what do you actually do about it?

What to buy

A-graders. But A-graders bought within a sensible price band — not at any price.

By definition, a home is only an A-grader if all three Ps, price included, are blue chip. So if you’re paying double the median for the area on a brand-new home that history says will depreciate — stop and ask yourself, honestly: is that the right decision?

Ten years ago, our line was simple. Buy well, live free. The harder question now is the other one: buy poorly, and how much is it costing you?

Here’s a rough way to see it. The numbers are round, but the shape is real.

Picture a $6 million home that current history says could be worth $5 million in ten years.

Borrow half — $3 million at 6% — and that’s $180,000 a year in interest. And because this is your home, that interest isn’t tax-deductible: to pay $180,000 out of your own pocket, a top-rate earner has to earn closer to $340,000 before tax. So call it $340,000 a year — $3.4 million — simply to service that loan for a decade.

Now add the opportunity cost on the $3 million of your own money tied up in it — roughly $2.3 million it could have earned elsewhere over ten years. Then add the $1 million the home itself has lost.

$3.4 million, plus $2.3 million, plus $1 million. That’s $6.7 million over ten years — about $55,000 a month to own a home that went backwards.

Of course, if it goes forward — as homes can — it’s a very different story. This is the cost of buying poorly.

Compare it to renting the same home. Say $10,000 a month — and because rent comes from after-tax income too, a top-rate earner needs about $19,000 before tax to cover it.

$55,000 against $19,000 each month.

Bottom line

Buy poorly and you don’t live free. You pay nearly three times the rent for the privilege of going backwards.

How to sell

Are you too focused on price — and too unfocused on actually selling?

Too lofty a goal, and too narrow a focus, not recognising the new paradigm the Melbourne top end is in.

Many sellers fix on a number from yesterday and miss the little things that actually win the day — the right people, the right process, the right price.

We see it all the time. Head down, or head in the sand. So focused on a price that no longer exists that they lose sight of the only thing that really matters: their life, moving forward. (And in truth, we’re no better on our own homes — which is exactly why process matters.)

Get the three Ps right — price, people, process — and the sale serves the life. Cling to yesterday’s price, and it does the opposite.

What we’re seeing across the market

The market today is not one market. It’s three, operating at once.

$1 million to $2 million. Still highly competitive. A and B-grade homes continue to attract multiple bidders, particularly quality family homes and turnkey stock.

$3 million to around $6 million. The most price-sensitive market in Melbourne right now. Buyers are active — but cautious. Deals happen only when pricing, presentation and negotiation strategy are aligned.

Above $7 million or a lot higher than your suburbs median price. Very thin. Buyers exist, but urgency largely doesn’t. Negotiations are elongated, decisions slower, and failed campaigns increasingly difficult to recover.

One note worth making: investors, developers, overseas buyers, expats and Chinese-Australians are very distinct markets — and in this segment, most of them left the building some time ago. So they’ll take far longer to show any post-budget effect.

This month @ James

This month we’ve been involved in buys across Beaumaris, Prahran, Ripponlea, Brighton, Parkville, Black Rock, Richmond, Surrey Hills, South Yarra, Hawthorn, Ivanhoe East, Albert Park and Camberwell.

Thirteen significant properties. We purchased six of them. Around $28 million worth, at an average price just under $4.7 million.

The homes we bought are below. They tell the story better than any clearance rate — A-graders and the rest, buyers and sellers, in the new market we’ve described across this report.

And if you’re weighing a move — buying or selling — and you’d value a frank, unhurried conversation rather than a sales pitch, we’re always glad to talk quietly.

Mal James 0408 107 988 and Simone Clarke 0400 304 111

PS We’ll keep working through the King’s Birthday weekend and beyond (Go Pies!), with each of us taking a little holiday along the way. Mine is rock climbing in the Dolomites, in Italy and some other treks in the arctic and the Matterhorn — so if I survive, I’ll see you in the next due Marketnews, in early Spring.

James Buy Sell is launching multi-agent campaigns across Aspendale (beachfront), Balwyn (a cute sub-$3m home), Canterbury (reno-or-rebuild, sub-$3m, on a great block), Prahran (one or two homes in one, sub-$3m), Brighton (a block of land on Halifax Street, sub-$3m), South Yarra (a brilliant four-bedder, sub-$3m), Camberwell (a substantial, ready-to-move-in family home, $8m), East Melbourne (a large family home) — and more.

And a sample of what we’re still looking to buy: Ivanhoe East (a $2.5m family home), Armadale (a Victorian on good land, $7m), Boroondara (a period home, up to $6m), and Richmond (circa $1.4m).

Homes James Buy Sell bought this month – real life Melbourne commentary

Well done A&I